Clean audit for GCSD, which took a hit with tax challenges and has a growing liability for future retirees’ health benefits

— Graphs from West & Company CPAs audit

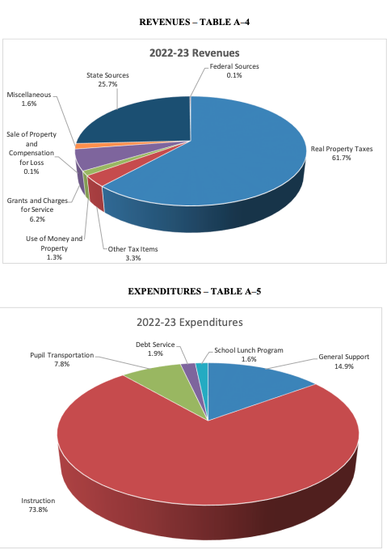

Property taxes make up 62 percent of Guilderland school revenues, at top, while state aid accounts for 26 percent. Transportation costs grew to nearly 8 percent in 2022-23 while instruction still accounts for the lion’s share of spending at nearly three-quarters.

GUILDERLAND — The school board here accepted another clean audit on Tuesday, which has the same drawback as other districts face — growing liabilities for future retirees’ health benefits — as well as adjustment for the large tax challenges the district had to make good on.

“This is a clean or unmodified audit opinion so that is the highest that you can receive,” Jill M. Thaisz, a certified public accountant and partner at West & Company CPAs, told the board.

She walked the board members through her company’s 74-page audit and answered their questions during the board’s Oct. 3 meeting.

The audit notes that Guilderland lost about $5 million in net position due larging to increased costs for pupil transportation and tax certiorari expenditures as well as an increase in net pension liabilities.

It also notes that the school budget passed by 65.5 percent in May 2022, and that the district’s total assessed valuation decreased by approximately $77 million or 1.8 percent in 2022-23 showing a slight decrease from the prior year but “indicating an overall stable tax base and economic stability.”

Thaisz noted total assets of $161 million, the largest component being capital assets like land, buildings, and equipment.

The district has total liabilities of just under $308 million; the largest liability is post-employment benefits.

“All school districts are required to have an actuary estimate of the district’s future cost to provide retiree health insurance …,” said Thaisz. “But New York state does not allow you to set any fund aside to pay the future liability; each year, when you budget, you’re only allowed to budget for the current premiums.”

Thaisz said that, consequently, many districts have a large liability with no offsetting assets. Guilderland, she said, has a deficit of $172 million that it can’t fund.

Overall, Thaisz told the board members, “Your revenues were less than your expenses by $93,763 for the year.” However, she went on, “That is very good considering the fact that you had to pay out almost $3.4 million of tax certiorari claims this year, and your transportation expenses were also up.”

Comparing the district’s 2022-23 budget to its actual revenues for the year, Thaisz said, “Your use of money in property ended up much higher than budgeted, and that was thanks to increased interest rates, so you earned more on the money you held.”

Also, state aid was higher than budgeted.

Those higher revenues helped offset the added expenses for tax certiorari settlements. Many property owners, particularly businesses, challenged their assessed value after Guilderland went through a town-wide property revaluation.

The school district had originally budgeted $1.3 million for settling tax challenges but ended up having to spend $4.3 million.

Other than that, Thaisz noted, “There are very few large variances between what you budgeted and what you actually expended.”

Thaisz also noted that school districts are allowed to have up to 4 percent of next year’s budget in an unassigned fund balance, or rainy-day account, at the end of the year. “You’re right at the 4 percent so you’re all set there,” said Thaisz.

Because the district spent more than $750,000 in federal grant money, due to pandemic-related funding, two additional audit reports were required.

“These are two more clean, unmodified opinions,” said Thaisz. “The first one states that we did not find any material weaknesses in internal control and the second one states that you’re in compliance for the major program grants that we tested.”

The federal grants came with specific requirements on how schools could spend the funds in the wake of the shutdowns caused by COVID-19.

Thaisz also noted that Guilderland got about $818,000 from the United State Department of Agriculture, down substantially from last year when free meals were provided for all students at a higher reimbursement rate.

Just at it did last year, Guilderland received a “qualified opinion” on its fiscal oversight of “extra-classroom” finances, that is, club money.

Her company gives a qualified opinion for club money to all the districts it audits because, Thaisz said, “We can’t prove that all of the money raised is submitted to the central treasurer.”

John Rizzo, the district’s school business administrator, said last year when the same issue was raised, that, when a club has been financially inactive for three years, after he has communicated with the club’s advisor, any money that club has is rolled into the student government account.

“Some clubs are active without financial activity,” said Rizzo. In those cases, he encourages them to raise a dollar “to comply with the literal letter of the law.”

“Otherwise,” Thaisz concluded on Tuesday, “everything that we tested looked good.”

a President Seema Rivera checked on the fact that the large liability for post-employment benefits cannot be helped by the district.

“You are required by the Governmental Accounting Standards Board to record the liability,” confirmed Thaisz. “So all districts are required to record the liability. But New York state has not set up any type of reserve for you to be able to fund the liability.”

“So you can’t save for that, so this is always going to be in a deficit?” asked Rivera.

“Unless New York somehow decides that they’re going to change their mind,” said Thaisz, concluding “We’ve seen no signs of that yet.”